After the end of the Cold War, General Dynamics performed poorly, with revenues of $10 billion and a market capitalization of just $1 billion, along with $600 million in debt. GD primarily produces aircraft, tanks, ships, and land vehicles, such as tanks, for the Pentagon. Bill Anders became CEO of GD in 1991.

He was already known for his role in the Apollo 8 mission, where he took the iconic "Earthrise" picture, and he was an air force fighter pilot with a degree in nuclear engineering. Having succeeded Jack Welch, he described GD in the following way: "There was a terrific group of GE managers who were excellent swimming instructors . . . although they occasionally tried to drown you."

This was his strategy for turning around GD:

Anders, taking a page from his former GE colleague Welch, believed that General Dynamics should only engage in businesses where it held the number one or number two market position. (This approach bore a striking resemblance to the Powell Doctrine of the same era, advocating that the United States should only enter military conflicts it could decisively win.)

The company would divest from commodity businesses where returns were unacceptably low.

It would adhere to businesses it knew well, being cautious about commercial ventures—a long-pursued, holy grail-like source of new profits for defense companies.

He replaced twenty-one of the company’s top twenty-five executives.

Bill Anders was CEO for only three years. His tenure can be divided into two parts: the generation of cash and its deployment. He turned around the cash flow, shifting it from negative to making $5 billion in the following three years.

Remarkable tightening of operations included:

Removing massive overinvestment in inventory, capital equipment, and research and development.

Cutting inventory.

Strongly emphasizing ROI: "Cash return on capital became the key metric within the company and was always on our minds."

Only bidding for really good government contracts and being selective.

Reducing headcount by 60% (corporate staff by 80%).

Reducing investment in working capital. Mellor mentioned, "For the first couple of years, we didn’t need to spend anything; we could simply run off the prior years’ buildup of inventories and capital expenditures."

These strategic actions led to the company becoming a leader in Return on Assets (ROA), a position it still holds today.

The sale of non-core businesses included:

Selling the majority stake of GD IT division, the Cessna aircraft business, and the missiles and electronics businesses.

Selling GD’s F-16 business to Lockheed for $1.5 billion.

These moves resulted in the company shrinking in size but growing per share value. Now, having the opportunity to fly the jets himself, Bill Anders was rational, pragmatic, agnostic, and clear-eyed. He had left the tanks and submarines business behind.

Capital allocation:

Due to high prices, he decided not to acquire further companies; instead, he returned value to shareholders.

Three special dividends were issued.

A $1 billion tender was launched to repurchase 30% of shares.

He generated shareholder value by shrinking the company itself: "Most CEOs grade themselves on size and growth... very few really focus on shareholder returns."

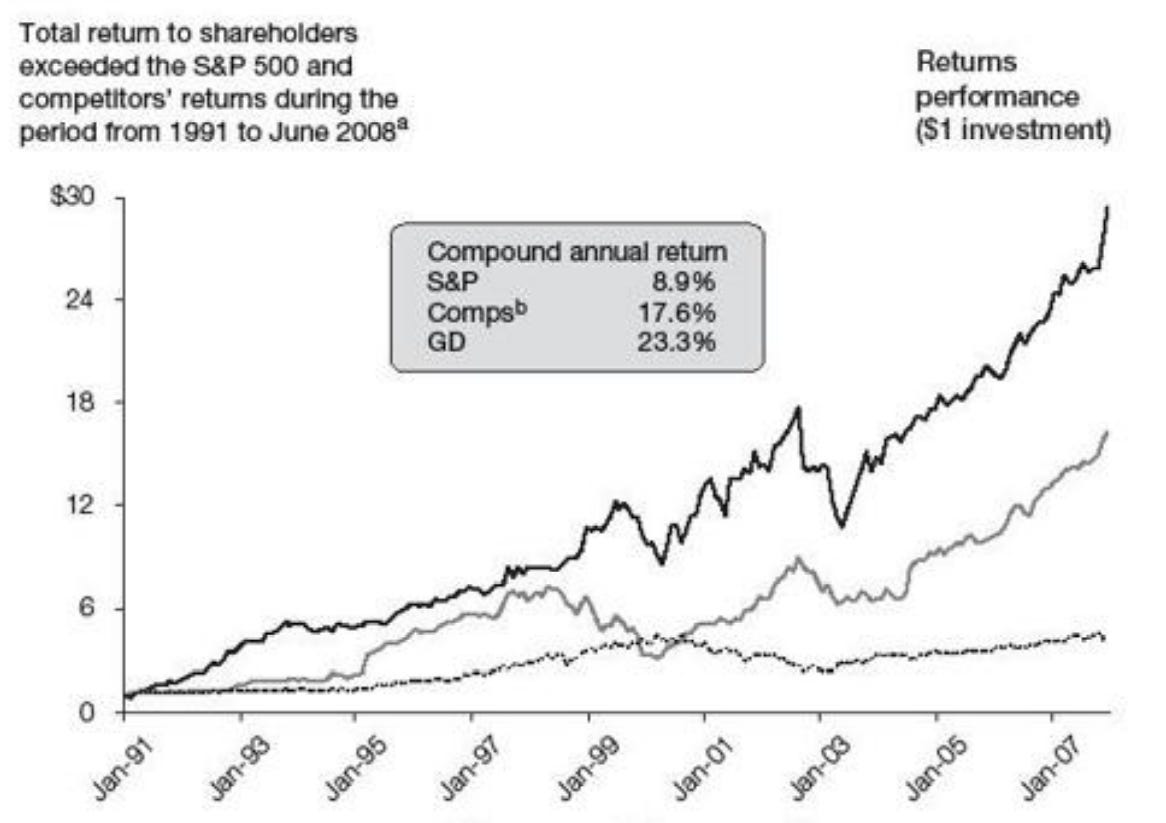

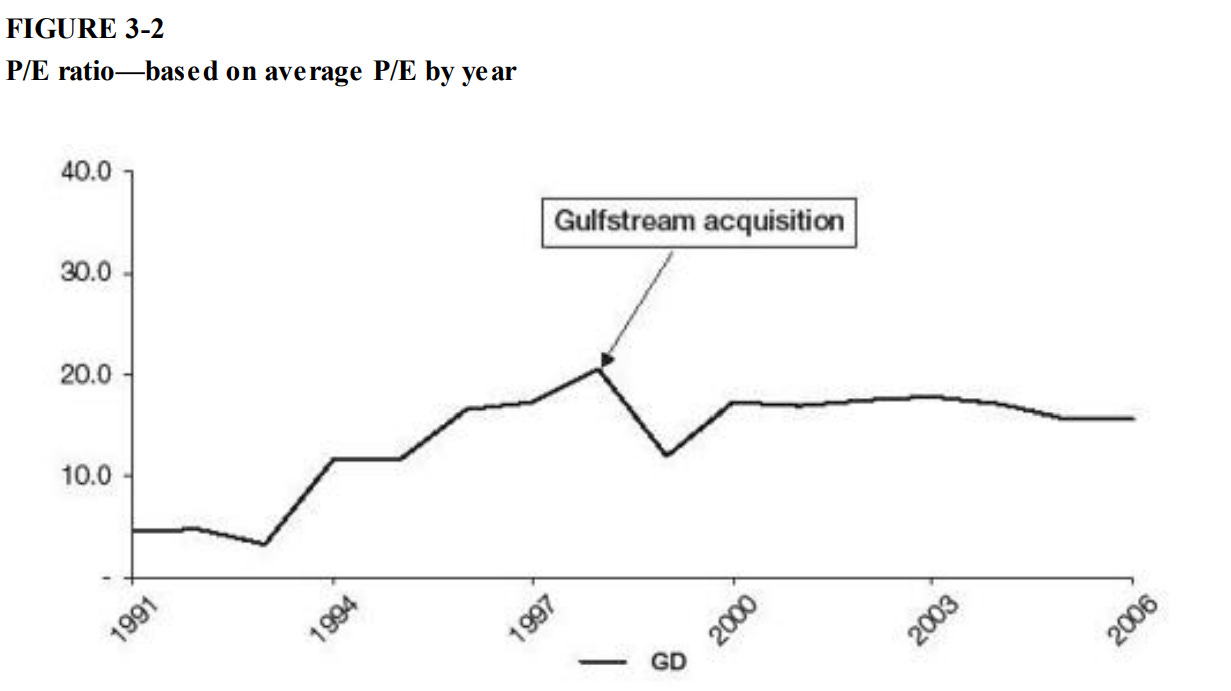

Anders left in July 1993, and Mellor became CEO. While Mellor continued to sell smaller divisions, he halted rumors that "the company would be completely liquidated" by purchasing Bath Iron Works for $400 million. When he retired, Nick Chabraja became CEO in 1997. In 1999, he acquired Gulfstream for $5 billion, representing 56% of GD EV. The rationale behind this acquisition was GD's expertise in aviation and to counterbalance the defense sector's fluctuations. Until his retirement in 2008, he achieved extraordinary performance.

23,3% compound annual return vs 8,9% for the S&P500 vs 17,6% for peers

Key Principles in Human Resources:

Decentralizing: Distributing responsibilities and decision-making throughout the organization.

Aligning management compensation with shareholders’ interests: Ensuring that the interests of management are in line with those of the shareholders.

Pushing responsibility further down into the organization: Empowering lower levels of the organization with decision-making authority.

Eliminating layers of middle management: Streamlining the organizational structure by reducing unnecessary middle management.

Removing corporate headquarters staff extensively: Reducing the size and scope of corporate headquarters personnel.

Only two people between the CEO and the head of any profit center: Maintaining a flat organizational structure to enhance communication and decision-making.

Eliminating or pushing down human relations, legal, and accounting personnel at headquarters: Reducing centralized support functions and pushing them closer to operating divisions.

Holding operating managers responsible for hitting their budgets and leaving them alone if they did so: Emphasizing accountability and autonomy for achieving budgetary goals.

Implementing performance-based compensation tied to stock price: Rewarding employees based on the company's stock performance.

Key Principles in Human Resources:

GD did not really need to raise any capital due to the sale of several divisions. However, this was different in the Gulfstream acquisition. Nick sold stock, equating to one-third of the entire company. He only sold stock due to its high P/E.

“Nick sold shares equaling one-third of the company to acquire a business that provided half of our consolidated operating cash flow.” The best capital allocators are practical, opportunistic, and flexible.

When his peers were engaging in acquisition binge, he was selling, giving out dividends, and repurchasing shares –> Contrarian.

Selective acquisitions.

Spending meaningfully less money on capital expenditures and paying lower dividends than his peers while devoting substantial resources to acquisitions and sporadic stock repurchases.

Thinking like an investor: “We bought heavily when we thought we could take advantage of market mistakes in pricing our stock.”

Not overemphasizing revenue growth.

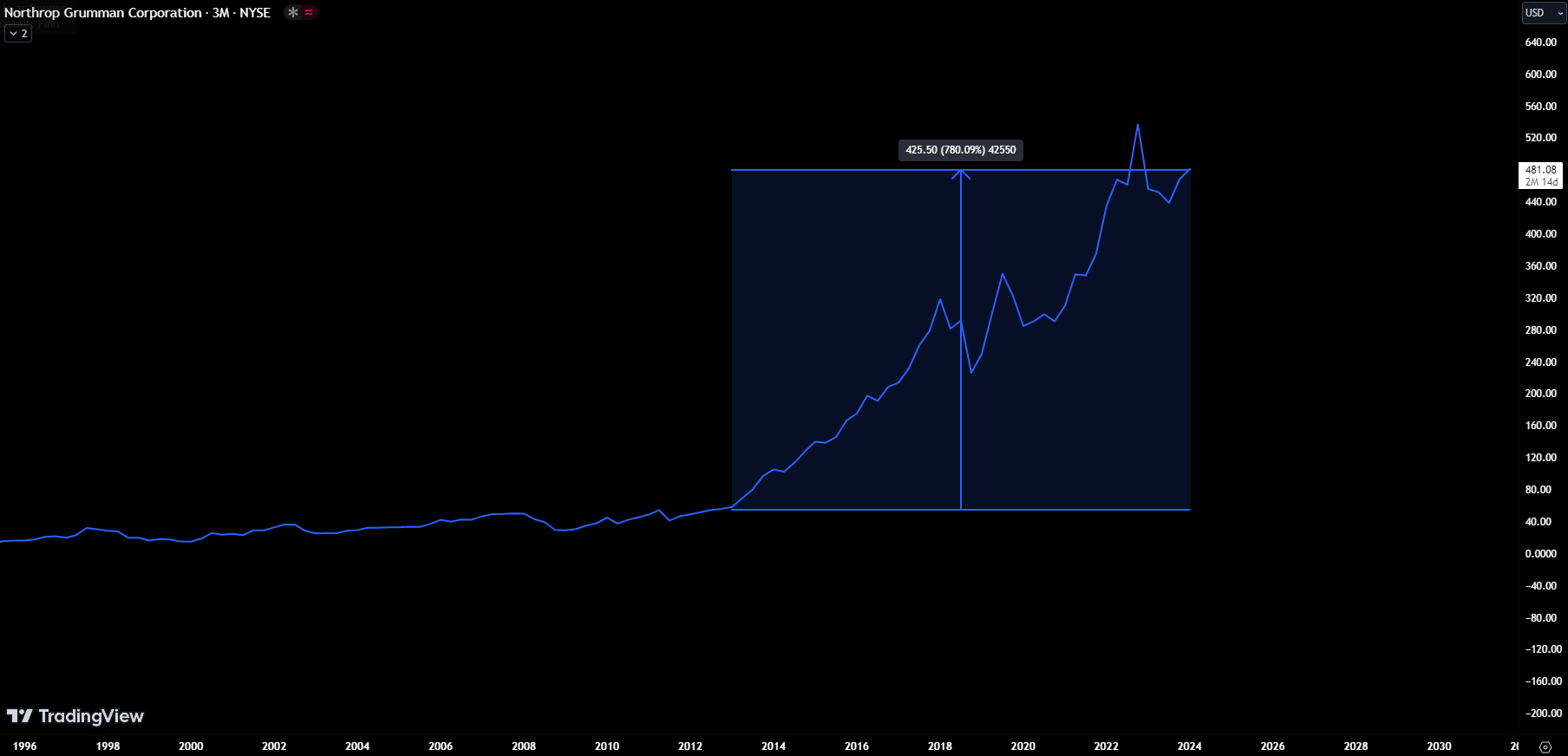

Like in Part 1 where I talked about TDG 0.00%↑ copying Capital Cities, Northrop Grumman's CEO said in 2012 (when the book came out) that the next steps will be the same ones taken like GD did in the 90s.

Most of the informations is taken from the book The Outsiders.